ЪБМфађСаФЃаЭИљОнбаОПЖдЯѓЪЧЗёЫцЛњЗжЮЊШЗЖЈадФЃаЭКЭЫцЛњадФЃаЭСНДѓРрЁЃ

ЫцЛњЪБМфађСаФЃаЭМДЪЧжИНігУЫќЕФЙ§ШЅжЕМАЫцЛњШХЖЏЯюЫљНЈСЂЦ№РДЕФФЃаЭ,НЈСЂОпЬхЕФФЃаЭ,ашНтОіШчЯТШ§ИіЮЪЬтФЃаЭЕФОпЬхаЮЪНЁЂЪБађБфСПЕФжЭКѓЦквдМАЫцЛњШХЖЏЯюЕФНсЙЙЁЃ

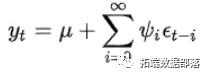

ІЬЪЧytЕФОљжЕЃЛІзЪЧЯЕЪ§ЃЌОіЖЈСЫЪБМфађСаЕФЯпадЖЏЬЌНсЙЙЃЌвВБЛГЦЮЊШЈжиЃЌЦфжаІз0=1ЃЛ{ІХt}ЮЊИпЫЙАздыЩљађСаЃЌЫќБэЪОЪБМфађСа{yt}дкtЪБПЬГіЯжСЫаТЕФаХЯЂЃЌЫљвдІХtГЦЮЊЪБПЬtЕФinnovationЃЈаТаХЯЂЃЉЛђshockЃЈШХЖЏЃЉЁЃ

ЕЅЮЛИљВтЪдЪЧЦНЮШадМьбщЕФЬиЪтЗНЗЈЁЃЕЅЮЛИљМьбщЪЧЖдЪБМфађСаНЈСЂARMAФЃаЭЁЂARIMAФЃаЭЁЂБфСПМфЕФаећЗжЮіЁЂвђЙћЙиЯЕМьбщЕШЕФЛљДЁЁЃ

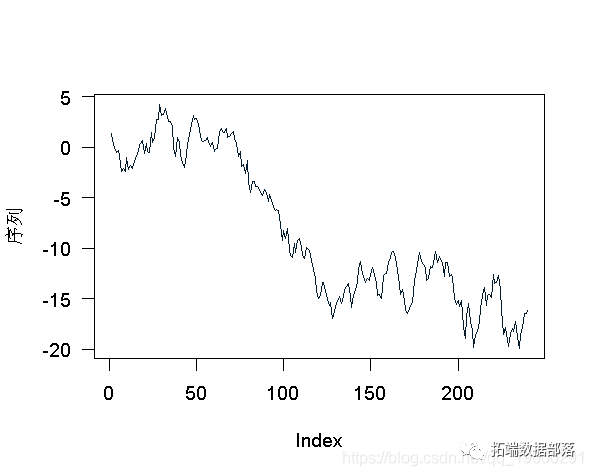

ЖдгкЕЅЮЛИљВтЪдЃЌЮЊСЫЫЕУїетаЉВтЪдЕФЪЕЯжЃЌПМТЧвдЯТЯЕСа

> plot(X,type="l")

- Dickey FullerЃЈБъзМЃЉ

етРяЃЌЖдгкDickey-FullerВтЪдЕФМђЕЅАцБОЃЌЮвУЧМйЩш

ЮвУЧЯыВтЪдЪЧЗёЃЈЛђВЛЪЧЃЉЁЃЮвУЧПЩвдНЋвдЧАЕФБэЪОаДЮЊ

ЫљвдЮвУЧжЛашВтЪдЯпадЛиЙщжаЕФЛиЙщЯЕЪ§ЪЧЗёЮЊПеЁЃетПЩвдЭЈЙ§бЇЩњtМьбщРДЭъГЩЁЃШчЙћЮвУЧПМТЧЧАУцЕФФЃаЭУЛгаЯпадЦЏвЦЃЌЮвУЧБиаыПМТЧЯТУцЕФЛиЙщ

Call: lm(formula = z.diff ~ 0 + z.lag.1) Residuals: Min 1Q Median 3Q Max -2.84466 -0.55723 -0.00494 0.63816 2.54352 Coefficients: Estimate Std. Error t value Pr(>|t|) z.lag.1 -0.005609 0.007319 -0.766 0.444 Residual standard error: 0.963 on 238 degrees of freedom Multiple R-squared: 0.002461, Adjusted R-squared: -0.00173 F-statistic: 0.5873 on 1 and 238 DF, p-value: 0.4442

ЮвУЧЕФВтЪдГЬађНЋЛљгкбЇЩњtМьбщЕФжЕЃЌ

> summary(lm(z.diff~0+z.lag.1 ))$coefficients[1,3] [1] -0.7663308

ете§ЪЧМЦЫуЪЙгУЕФжЕ

ur.df(X,type="none",lags=0) ############################################################### # Augmented Dickey-Fuller Test Unit Root / Cointegration Test # ############################################################### The value of the test statistic is: -0.7663

ПЩвдЪЙгУСйНчжЕЃЈ99%ЁЂ95%ЁЂ90%ЃЉРДНтЪЭИУжЕ

> qnorm(c(.01,.05,.1)/2) [1] -2.575829 -1.959964 -1.644854

ШчЙћЭГМЦСПГЌЙ§етаЉжЕЃЌФЧУДађСаОЭВЛЪЧЦНЮШЕФЃЌвђЮЊЮвУЧВЛФмОмОјетбљЕФМйЩшЁЃЫљвдЮвУЧПЩвдЕУГіНсТлЃЌгавЛИіЕЅЮЛИљЁЃЪЕМЪЩЯЃЌетаЉСйНчжЕЪЧЭЈЙ§

############################################### # Augmented Dickey-Fuller Test Unit Root Test # ############################################### Test regression none Call: lm(formula = z.diff ~ z.lag.1 - 1) Residuals: Min 1Q Median 3Q Max -2.84466 -0.55723 -0.00494 0.63816 2.54352 Coefficients: Estimate Std. Error t value Pr(>|t|) z.lag.1 -0.005609 0.007319 -0.766 0.444 Residual standard error: 0.963 on 238 degrees of freedom Multiple R-squared: 0.002461, Adjusted R-squared: -0.00173 F-statistic: 0.5873 on 1 and 238 DF, p-value: 0.4442 Value of test-statistic is: -0.7663 Critical values for test statistics: 1pct 5pct 10pct tau1 -2.58 -1.95 -1.62

RгаМИИіАќПЩвдгУгкЕЅЮЛИљВтЪдЁЃ

Augmented Dickey-Fuller Test data: X Dickey-Fuller = -2.0433, Lag order = 0, p-value = 0.5576 alternative hypothesis: stationary

етРяЛЙгавЛИіМьбщСуМйЩшЪЧДцдкЕЅЮЛИљЁЃЕЋЪЧpжЕЪЧЭъШЋВЛЭЌЕФЁЃ

p.value [1] 0.4423705 testreg$coefficients[4] [1] 0.4442389

- діЙуDickey-FullerМьбщ

ЛиЙщжаПЩФмгавЛаЉжЭКѓЯжЯѓЁЃР§ШчЃЌЮвУЧПЩвдПМТЧ

ЭЌбљЃЌЮвУЧашвЊМьВщвЛИіЯЕЪ§ЪЧЗёЮЊСуЁЃетПЩвдгУбЇЩњtМьбщРДзіЁЃ

> summary(lm(z.diff~0+z.lag.1+z.diff.lag )) Call: lm(formula = z.diff ~ 0 + z.lag.1 + z.diff.lag) Residuals: Min 1Q Median 3Q Max -2.87492 -0.53977 -0.00688 0.64481 2.47556 Coefficients: Estimate Std. Error t value Pr(>|t|) z.lag.1 -0.005394 0.007361 -0.733 0.464 z.diff.lag -0.028972 0.065113 -0.445 0.657 Residual standard error: 0.9666 on 236 degrees of freedom Multiple R-squared: 0.003292, Adjusted R-squared: -0.005155 F-statistic: 0.3898 on 2 and 236 DF, p-value: 0.6777 coefficients[1,3] [1] -0.7328138

ИУжЕЪЧЪЙгУ

> df=ur.df(X,type="none",lags=1) ############################################### # Augmented Dickey-Fuller Test Unit Root Test # ############################################### Test regression none Call: lm(formula = z.diff ~ z.lag.1 - 1 + z.diff.lag) Residuals: Min 1Q Median 3Q Max -2.87492 -0.53977 -0.00688 0.64481 2.47556 Coefficients: Estimate Std. Error t value Pr(>|t|) z.lag.1 -0.005394 0.007361 -0.733 0.464 z.diff.lag -0.028972 0.065113 -0.445 0.657 Residual standard error: 0.9666 on 236 degrees of freedom Multiple R-squared: 0.003292, Adjusted R-squared: -0.005155 F-statistic: 0.3898 on 2 and 236 DF, p-value: 0.6777 Value of test-statistic is: -0.7328 Critical values for test statistics: 1pct 5pct 10pct tau1 -2.58 -1.95 -1.62

ЭЌбљЃЌвВПЩвдЪЙгУЦфЫћАќЃК

Augmented Dickey-Fuller Test data: X Dickey-Fuller = -1.9828, Lag order = 1, p-value = 0.5831 alternative hypothesis: stationary

НсТлЪЧвЛбљЕФЃЈЮвУЧгІИУОмОјађСаЪЧЦНЮШЕФМйЩшЃЉЁЃ

- ДјЧїЪЦКЭЦЏвЦЕФдіЙуDickey-FullerМьбщ

ЕНФПЧАЮЊжЙЃЌЮвУЧЕФФЃаЭжаЛЙУЛгаАќРЈЦЏвЦЁЃЕЋКмМђЕЅЃЈетНЋБЛГЦЮЊЧАвЛЙ§ГЬЕФРЉГфАцБОЃЉЃКЮвУЧжЛашвЊдкЛиЙщжаАќКЌвЛИіГЃЪ§ЃЌ

> summary(lm) Residuals: Min 1Q Median 3Q Max -2.91930 -0.56731 -0.00548 0.62932 2.45178 Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 0.29175 0.13153 2.218 0.0275 * z.lag.1 -0.03559 0.01545 -2.304 0.0221 * z.diff.lag -0.01976 0.06471 -0.305 0.7603 --- Signif. codes: 0 ЁЎ***ЁЏ 0.001 ЁЎ**ЁЏ 0.01 ЁЎ*ЁЏ 0.05 ЁЎ.ЁЏ 0.1 ЁЎ ЁЏ 1 Residual standard error: 0.9586 on 235 degrees of freedom Multiple R-squared: 0.02313, Adjusted R-squared: 0.01482 F-statistic: 2.782 on 2 and 235 DF, p-value: 0.06393

ПМТЧЕНЗНВюЪфГіЕФвЛаЉЗжЮіЃЌетРяЛёЕУСЫИааЫШЄЕФЭГМЦЪ§ОнЃЌЦфжаИУФЃаЭгыУЛгаМЏГЩВПЗжЕФФЃаЭНјааСЫБШНЯЃЌвдМАЦЏвЦЃЌ

> summary(lmcoefficients[2,3] [1] -2.303948 > anova(lm$F[2] [1] 2.732912

етСНИіжЕвВЪЧЭЈЙ§

ur.df(X,type="drift",lags=1) ############################################### # Augmented Dickey-Fuller Test Unit Root Test # ############################################### Test regression drift Residuals: Min 1Q Median 3Q Max -2.91930 -0.56731 -0.00548 0.62932 2.45178 Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 0.29175 0.13153 2.218 0.0275 * z.lag.1 -0.03559 0.01545 -2.304 0.0221 * z.diff.lag -0.01976 0.06471 -0.305 0.7603 --- Signif. codes: 0 ЁЎ***ЁЏ 0.001 ЁЎ**ЁЏ 0.01 ЁЎ*ЁЏ 0.05 ЁЎ.ЁЏ 0.1 ЁЎ ЁЏ 1 Residual standard error: 0.9586 on 235 degrees of freedom Multiple R-squared: 0.02313, Adjusted R-squared: 0.01482 F-statistic: 2.782 on 2 and 235 DF, p-value: 0.06393 Value of test-statistic is: -2.3039 2.7329 Critical values for test statistics: 1pct 5pct 10pct tau2 -3.46 -2.88 -2.57 phi1 6.52 4.63 3.81

ЮвУЧЛЙПЩвдАќРЈвЛИіЯпадЧїЪЦЃЌ

> temps=(lags+1):n lm(z.diff~1+temps+z.lag.1+z.diff.lag ) Residuals: Min 1Q Median 3Q Max -2.87727 -0.58802 -0.00175 0.60359 2.47789 Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 0.3227245 0.1502083 2.149 0.0327 * temps -0.0004194 0.0009767 -0.429 0.6680 z.lag.1 -0.0329780 0.0166319 -1.983 0.0486 * z.diff.lag -0.0230547 0.0652767 -0.353 0.7243 --- Signif. codes: 0 ЁЎ***ЁЏ 0.001 ЁЎ**ЁЏ 0.01 ЁЎ*ЁЏ 0.05 ЁЎ.ЁЏ 0.1 ЁЎ ЁЏ 1 Residual standard error: 0.9603 on 234 degrees of freedom Multiple R-squared: 0.0239, Adjusted R-squared: 0.01139 F-statistic: 1.91 on 3 and 234 DF, p-value: 0.1287 > summary(lmcoefficients[3,3] [1] -1.98282 > anova(lm$F[2] [1] 2.737086

ЖјRКЏЪ§ЗЕЛи

ur.df(X,type="trend",lags=1) ############################################### # Augmented Dickey-Fuller Test Unit Root Test # ############################################### Test regression trend Residuals: Min 1Q Median 3Q Max -2.87727 -0.58802 -0.00175 0.60359 2.47789 Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 0.3227245 0.1502083 2.149 0.0327 * z.lag.1 -0.0329780 0.0166319 -1.983 0.0486 * tt -0.0004194 0.0009767 -0.429 0.6680 z.diff.lag -0.0230547 0.0652767 -0.353 0.7243 --- Signif. codes: 0 ЁЎ***ЁЏ 0.001 ЁЎ**ЁЏ 0.01 ЁЎ*ЁЏ 0.05 ЁЎ.ЁЏ 0.1 ЁЎ ЁЏ 1 Residual standard error: 0.9603 on 234 degrees of freedom Multiple R-squared: 0.0239, Adjusted R-squared: 0.01139 F-statistic: 1.91 on 3 and 234 DF, p-value: 0.1287 Value of test-statistic is: -1.9828 1.8771 2.7371 Critical values for test statistics: 1pct 5pct 10pct tau3 -3.99 -3.43 -3.13 phi2 6.22 4.75 4.07 phi3 8.43 6.49 5.47

- KPSS Мьбщ

дкетРяЃЌдкKPSSЙ§ГЬжаЃЌПЩвдПМТЧСНжжФЃаЭЃКЦЏвЦФЃаЭЛђЯпадЧїЪЦФЃаЭЁЃдкетРяЃЌСуМйЩшЪЧађСаЪЧЦНЮШЕФЁЃ

ДњТыЪЧ

ur.kpss(X,type="mu") ####################### # KPSS Unit Root Test # ####################### Test is of type: mu with 4 lags. Value of test-statistic is: 0.972 Critical value for a significance level of: 10pct 5pct 2.5pct 1pct critical values 0.347 0.463 0.574 0.73

дкетжжЧщПіЯТЃЌгавЛжжЧїЪЦ

ur.kpss(X,type="tau") ####################### # KPSS Unit Root Test # ####################### Test is of type: tau with 4 lags. Value of test-statistic is: 0.5057 Critical value for a significance level of: 10pct 5pct 2.5pct 1pct critical values 0.119 0.146 0.176 0.216

дйвЛДЮЃЌПЩвдЪЙгУСэвЛИіАќРДЛёЕУЯрЭЌЕФМьбщЃЈЕЋЭЌбљЃЌВЛЭЌЕФЪфГіЃЉ

KPSS Test for Level Stationarity data: X KPSS Level = 1.1997, Truncation lag parameter = 3, p-value = 0.01 > kpss.test(X,"Trend") KPSS Test for Trend Stationarity data: X KPSS Trend = 0.6234, Truncation lag parameter = 3, p-value = 0.01

жСЩйгавЛжТадЃЌвђЮЊЮвУЧвЛжБОмОјМйЩшЁЃ

- Philipps-Perron Мьбщ

Philipps-PerronМьбщЛљгкADFЙ§ГЬЁЃДњТы

> PP.test(X) Phillips-Perron Unit Root Test data: X Dickey-Fuller = -2.0116, Truncation lag parameter = 4, p-value = 0.571

СэвЛжжПЩФмЕФЬцДњЗНАИЪЧ

> pp.test(X) Phillips-Perron Unit Root Test data: X Dickey-Fuller Z(alpha) = -7.7345, Truncation lag parameter = 4, p-value = 0.6757 alternative hypothesis: stationary

- БШНЯ

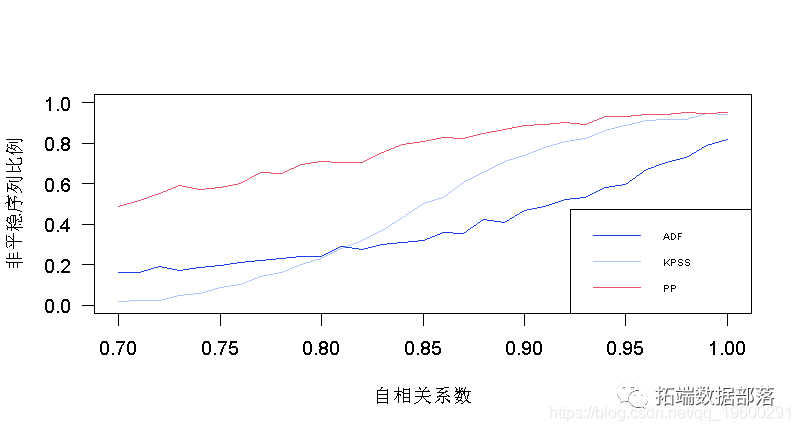

ЮвВЛЛсЛЈИќЖрЕФЪБМфБШНЯВЛЭЌЕФДњТыЃЌдкRжаЃЌдЫааетаЉВтЪдЁЃЮвУЧдйЛЈЕуЪБМфПьЫйБШНЯвЛЯТетШ§жжЗНЗЈЁЃШУЮвУЧЩњГЩвЛаЉЛђЖрЛђЩйОпгаздЯрЙиЕФздЛиЙщЙ§ГЬЃЌвдМАвЛаЉЫцЛњгЮзпЃЌШУЮвУЧПДПДетаЉМьбщЪЧШчКЮжДааЕФЃК

> for(i in 1:(length(AR)+1) + for(s in 1:1000){ + if(i!=1) X=arima.sim + M2[s,i]=(pp.testp.value) + M1[s,i]=(kpss.testp.value) + M3[s,i]=(adf.testp.value) + }

етРяЃЌЮвУЧвЊМЦЫуМьбщЕФpжЕГЌЙ§5%ЕФДЮЪ§ЃЌ

> plot(AR,P[1,],type="l",col="red",ylim=c(0,1) > lines(AR,P[2,],type="l",col="blue") > lines(AR,P[3,],type="l",col="green")

ЮвУЧПЩвддкетРяПДЕНDickey-FullerВтЪдЕФБэЯжгаЖрВЛЮШЖЈЃЌвђЮЊЮвУЧЕФздЛиЙщЙ§ГЬжага50%(жСЩй)БЛШЯЮЊЪЧЗЧЦНЮШЕФЁЃ